From the Editor: In part two of his series, author Kevin Smith takes us through the application of Enterprise Debt™ concepts (see Part 1) in the context of governance and lobbying in project execution.

Part 2 – GOVERNANCE AND LOBBYING OF PROJECT EXECUTION

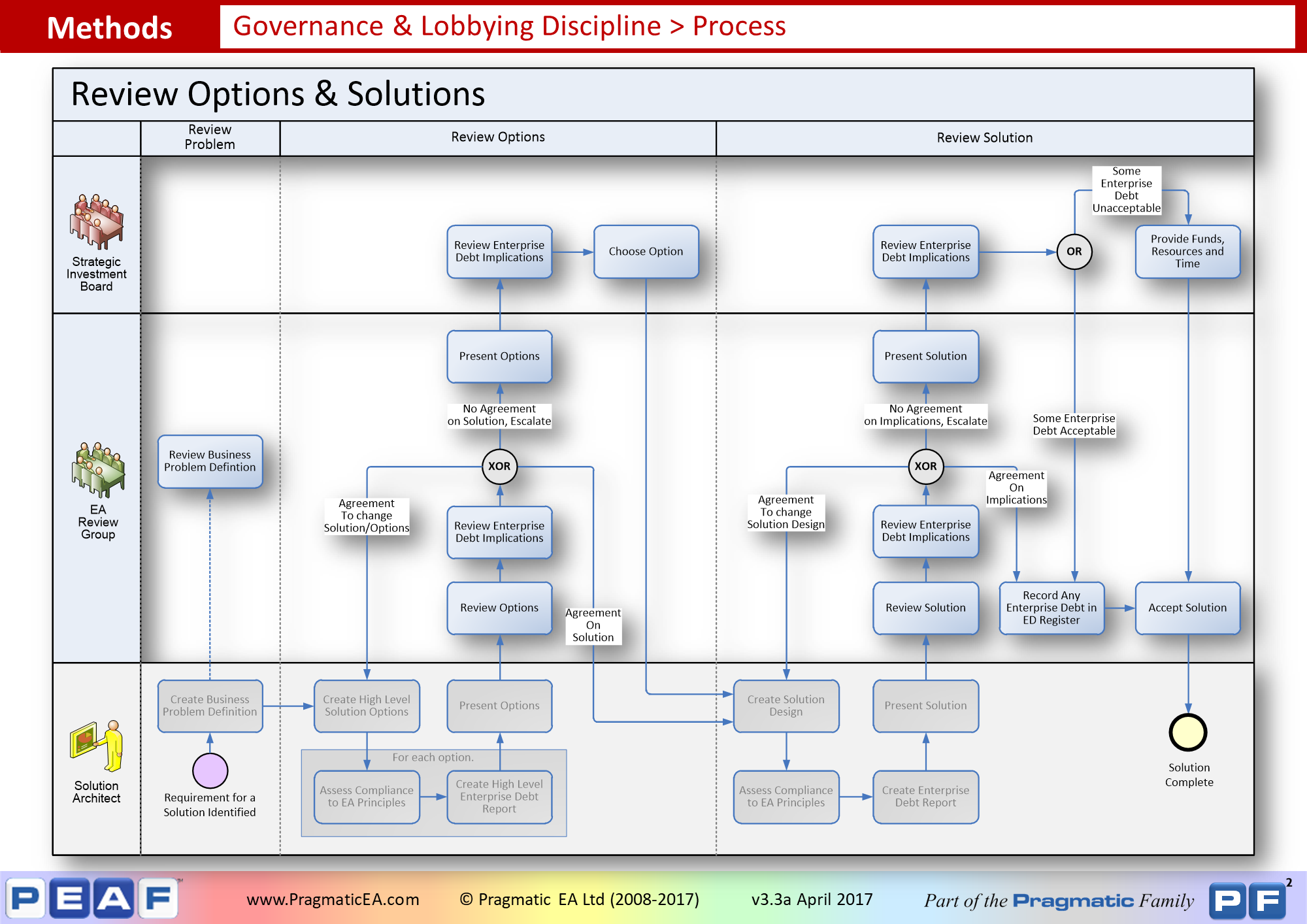

So let’s look at a specific example. Let us consider the Governance/Lobbying that is happening between the Roadmapping phase (the work done to formulate business and technical Structural roadmaps and Transformational roadmaps – a.k.a. a portfolio of projects) and the Elaboration phase (the work done at the start of all projects – commonly referred to as Solution Architecture) by considering the following diagram.

The work undertaken in any project can be thought of as consisting of three fundamental types:

- Compliant Work– Work that complies with Guidance. Generally the most effective, most efficient and least risky manner of achieving an end.

- Non-Compliant Work– Work that contravenes Guidance. Generally less effective, less efficient and more risky manner of achieving an end.

- Remedial Work– Work that exists to correct previous Tactical Work (i.e. changing previous Tactical work into Strategic Work)

Guidance here refers to the Structural (MACE) and Transformational (MAGMA) information dependant on the phase of the Transformation cascade we are in.

Note: Sometimes confusion can arise regarding whether a project is Tactical or Strategic. For example, a project might be deemed to be a Strategic Project (i.e. key for business success) but could be implemented solely by Tactical Work. This is the reason why in many projects, the project personnel may be raising red flags saying “This is a Tactical Project” while the Customer of the project may be saying “This is a Strategic Project”. WHY we are doing the project is Strategic, but HOW we are doing the project is Tactical. This is why many “Tactical Projects” end up being the “Strategic Solution”.

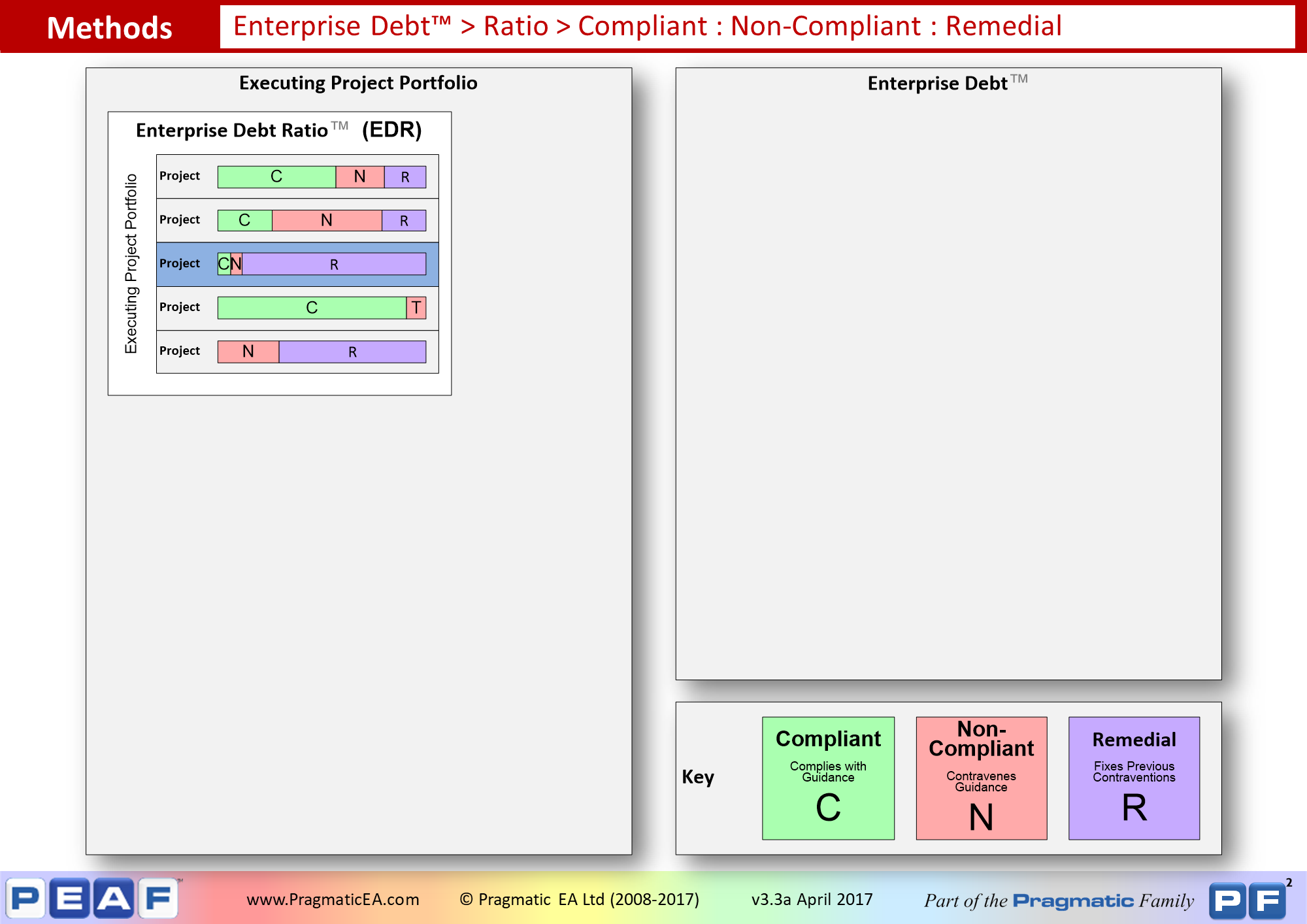

Here we see the Enterprise Debt Ratio™ (EDR) for the projects in the currently executing Project Portfolio. Enterprise Debt Ratio™ is the ratio (adding up to 1.0 or 100%) of Compliant vs Non-Compliant vs Remedial work in any project. Each project has a different ratio of Compliant vs Non-Compliant vs Remedial work.

Non-Compliant work is essentially a shortcut, and while a dictionary definition of a shortcut sounds quite positive and inviting:

1 : a route more direct than the one ordinarily taken

2 : a method or means of doing something more directly and quickly than and often not so thoroughly as by ordinary procedure <a shortcut to success>

– Merriam-Webster

In the business world the following is more true:

“A shortcut is the longest distance between two points.”

– Issawi’s Law of the Path of Progress

Add to this the following…

“Nothing is permanent, except for temporary solutions.”

– Jeroen van de Kamp

…and you can perhaps begin to see why Enterprises not only naturally decay into entropy over time but how uninformed management decisions actively encourage and hasten it.

Although Enterprise Debt Ratio™ is defined for each project, it can also be combined to produce an EDR for a group of projects in a program, or an overall EDR for the entire Project Portfolio. Of course, when combining EDR you need to weight each individual EDR to get a balanced view.

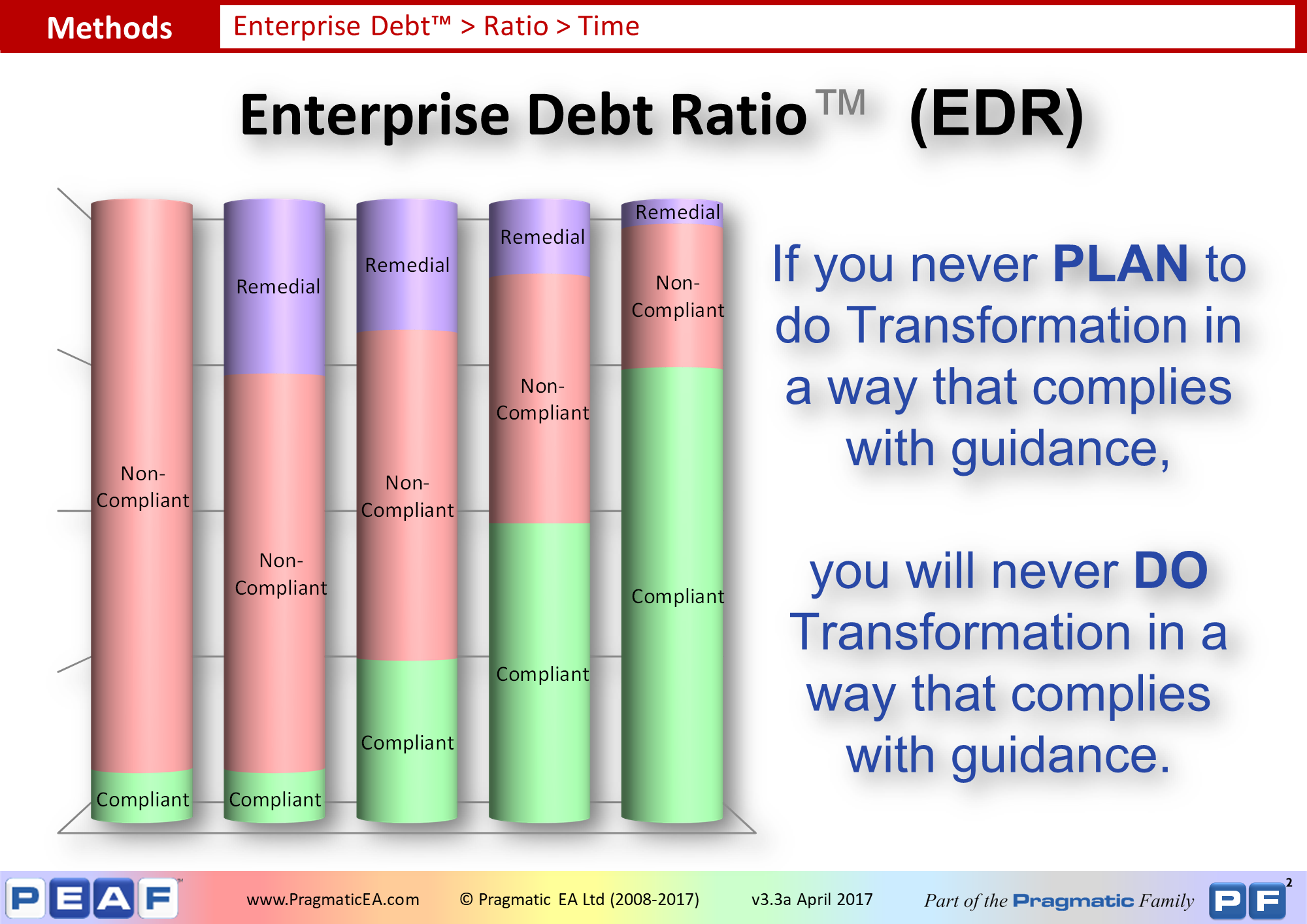

While Enterprise Debt Ratio™ for the entire Transformation Portfolio provides a useful metric at a point in time, it is more useful to track it over time. A sensible view might be that over time, an Enterprise might like to see the amount of work that is Compliant increase and the amount of work done in a Non-Compliant way decrease – since doing work in a Compliant way is generally the most effective, most efficient and least risky manner of doing it.

- In Year 0 – the year of adopting PEAF (and hence Enterprise Debt™) it is more than probable that a lot of work will still have to done in a Non-Compliant way. However we make the necessary plans to do a decent amount of Remedial work the following year.

- In Year 1, while still having to do a lot of work in a Non-Compliant way, we perform the Remedial work we planned the year before, which lays the groundwork for Year 2.

- In Year 2, we can now start to do more work in a Compliant way (because of the remedial work we did in the previous year) and less work in a Non-Compliant way, while still doing some Remedial work, both of which lays the groundwork for Year 3.

- In Year 3, doing work in a Compliant way is now beginning to outweigh doing work in a Non-Compliant way (because of the remedial and Compliant work we did in the previous year) and this, in addition to a little Remedial work, lays the groundwork for Year 4.

- In Year 4 we are doing most work in a Compliant way and only do work in a Non-Compliant way when really necessary.

This is only an example of course and will vary from Enterprise to Enterprise and will be influenced by many factors such as the fiscal climate and current Enterprise Strategy.

However, the examples provided illustrate one of the indicators of increasing EA Maturity, in that Enterprises that are more “mature” are the ones who spend a greater proportion of their resources doing work in a Compliant way rather than a Non-Compliant way and therefore need to spend little on remedial work.

The key point is:

If You Never PLAN To Do Transformation

In A Way That Complies With Guidance,

You Will Never DO Transformation

In A Way That Complies With Guidance.

Unless you planned for it, time pressures (the incessant need for quick wins for example) will always force you to do work in a Non-Complaint way, rather than in a Compliant way. The key is breaking the cycle.

Another thing to consider is that the choices being made when formulating the Transformation Portfolio should perhaps aim to do less, better. What we mean by that is that it might be a better approach to doing less things in a Compliant way (spending the money and time you save on allowing those initiatives to execute in a Compliant way (thereby incurring no Enterprise Debt™) rather than doing more things in a Non-Compliant way (thereby incurring Enterprise Debt™).

If the work in a project complies with all Guidance (aka is Compliant) then we have no problems. If not and some work does not comply with some Guidance (a.k.a. is Non-Compliant) then a Waiver is created. The waiver details three things:

- Cost of Compliance – What is preventing the project from complying with the guidance, and what does the project need to be given to allow the project to comply and therefore convert the work from Non-Compliant to Compliant.

- Cost of Non-Compliance – What issues and risks going forward will this Non-Compliance create for the Enterprise.

- Cost of Remediation – What will it cost the Enterprise to become Compliant in the future (assuming the project is not allowed to do what is required now to become Compliant).

In simple terms:

- The Cost of Compliance – What will it cost the project to do the right things now.

If the project is not granted the Cost of Compliance:

- The Cost of Non-Compliance – What pain will the Enterprise have to endure going forward, until we incur

- The Cost of Remediation – What will it cost the Enterprise later to fix it.

Having defined this information, a business decision can then be made to either provide what is required now or accept the pain we will have to endure going forward AND the costs of fixing it later. This is what sits at the heart of Governance and Lobbying.

Since a project that is Non-Compliant with guidance while the project is executing could become Compliant at any time before the project ends, only when a project completes will we know how many waivers have been issued and the Enterprise Debt™ being created in the form of the Cost of Non-Compliance that the Tactical work created and the Cost of Remediation to correct that Tactical work in the future.

At that point in time the Cost of Non-Compliance that the Non-Compliant work created, and the Cost of Remediation to correct that Non-Compliant work in the future, can be added to the Enterprise Debt™ for the whole Enterprise.

In effect the Cost of Non-Compliance is akin to paying interest on the Debt we have incurred, while the Cost of Remediation (if spent) is akin to paying off the Debt.

When you incur Enterprise Debt™, you are selling tomorrow, to get through today.

The steps in the bottom part of this process (in grey) are there to illustrate what work should be going on in a project as part of the Initiating phase. PEAF does not prescribe what these are (that is the job of PEEF – The Pragmatic Enterprise Engineering Framework), but we need to document them so we can show how Governance & Lobbying fits in, and also to make sure it fits in, in the correct way.

For more information on this topic, PEAF publish a book and have training courses available. You can get more information here. *

* Note: EAPJ helps to share information on EA-related courses provided by others, however these postings do not represent EAPJ’s endorsement of such opportunities.

In the “Entprise Debt->Value” picture, the completed work R (I assume remedial) increases Enterprise Debt, but I would have thought that such work would reduce Enterprise Debt? The completed work N would have two components, the “cost of compliance” and “cost of remediation” and these would increse the Enterprise Debt. Am I missing something, or has the colour purple been used to represent more than one thing (Remedial work in the project – ie, undoing previous non-compliance work – and the cost of remediation of the non-compliance work in that project?)

Hi David,

The part of the diagram you refer to is at the point in time when a project ends, and the reuslting Transformatino Debt is added to the overal Enterprise Debt. so at that point, the remedial work documented on the waiver is future work to be done – which is debt. When that identified remedial work is executed later (as show underneath the large ellipse) you are correct that at that point in time, it reduces Enterprise Debt.

Cheers,

Kevin.